USDA's Economic Research Service (ERS) provides a range of data products and reports on the wheat market—including domestic and international supply, demand, trade, and prices.

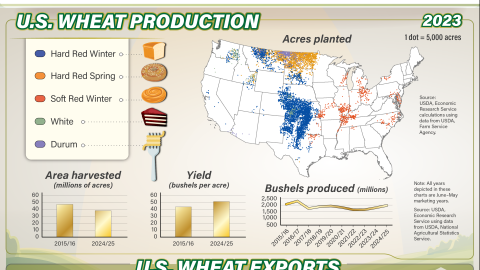

Wheat ranks third among U.S. field crops in planted acreage, production, and gross farm receipts—behind corn and soybeans. In marketing year 2025/26, U.S. farmers produced a total of 2.0 billion bushels of Winter, Durum, and Other Spring wheat from a harvested area of 37.2 million acres. The general downward trend in wheat plantings over the last four decades is attributable to lower relative returns for wheat, changes in Government programs that give farmers more planting flexibility, and increased competition in global wheat markets. However, wheat area increased slightly in 2023/24 as elevated prices provided an incentive to plant additional wheat.

The U.S. share of the global wheat market also declined over the past two decades, as the EU and Russia's shares increased. Between 2001/02 and 2005/06, the U.S. share of global wheat exports averaged 25 percent; for the 2025/26 marketing year, the U.S. share is projected at 11 percent.

Periodic and Scheduled Wheat-related Publications and Data

- The Wheat Outlook: A monthly report presenting supply and use projections for U.S. and global wheat markets, based on the current World Agricultural Supply and Demand Estimates.

- Wheat Data: A monthly data set showing statistics on U.S. supply and use of wheat including the five classes of wheat: (Hard Red Winter, Hard Red Spring, Soft Red Winter, White, and Durum) and rye.

- Wheat Data Visualization: An interactive tool that showcases various data series from the Wheat Yearbook tables.

- Feed Grains Database: A searchable database containing statistics on four feed grains (corn, grain sorghum, barley, and oats), foreign coarse grains (feed grains plus rye, millet, and mixed grains), wheat (and related feed byproducts), hay, and related feed market data. Data from the Feed Outlook and Feed Yearbook are also included.

- Commodity Cost and Returns: A data product that provides annual estimates of production costs and returns for major field crops, including corn and wheat.

- Agricultural Baseline Projections: An annual report published in February that offers 10-year projections for the farm sector from USDA's annual long-term analysis. The associated Baseline Database has projections for the four major feed grains (corn, sorghum, barley, and oats), in addition to the other major feed crops and livestock.

- Production, Supply, and Distribution (PS&D): This database contains official USDA data on production, supply, and distribution of agricultural commodities for the United States and major importing and exporting countries. The database provides by country projections for the coming year and historical data for major crop and livestock products.

Selected ERS Wheat-related Reports

In addition to the periodic Outlook reports and data products, ERS publishes reports covering issues important to wheat markets in the United States and globally.

Selected ERS reports, special articles, and features relating to wheat include:

- “U.S. Census of Agriculture: Highlighting Changing Trends in Wheat Farming” in Wheat Outlook: March 2024: This article provides perspective on changing dynamics of the wheat farming sector, using data from the Census of Agriculture, published by USDA, National Agricultural Statistics Service (NASS).

- "Import Code Allocation Changed in Response to New Trade Flows” in Wheat Outlook: November 2023: This article provides background context on recent imports from the European Union to explain a revision to U.S. by-class import allocations.

- “Changes in Ukraine Wheat and Corn Export Patterns Since the Start of the Ukraine-Russia War” in Wheat Outlook: January 2023: This article provides analysis of the changing patterns of Ukraine’s exports since the start of the war, including impacts on importing markets.

- “Rail Transportation Challenges Among Major Factors Weighing on U.S. Wheat Exports” in Wheat Outlook: December 2022: This article provides a perspective of major factors impacting U.S. wheat exports for the 2022/23 marketing year. The article highlights the role that rail transportation plays in the U.S. wheat industry and discusses the potential ramifications of service delays.

- “Wheat By-Class Trade Estimation Methods” in Wheat Outlook: October 2022: This article provides detailed descriptions of the conversion factors used in calculating wheat trade data and allocating the data across the five classes.

- “Factors Influencing Prevented Planting for Spring Wheat” in Wheat Outlook: September 2022: This article describes the planting conditions for spring wheat in 2022 and the market conditions influencing producer decisions.

- “Country Focus: India” in Wheat Outlook: June 2022: This article provides a historical view of India’s wheat market along with discussion of its recently imposed export ban.

- “U.S. Wheat Pricing and Exports in 2021/22” in Wheat Outlook: April 2022: This article explains the key market considerations that have impacted exports of U.S. wheat classes in 2021/22.

- Evolution of Russian Wheat Export Restrictions and Potential Impacts” in Wheat Outlook: February 2022: This article provides a historic view of wheat Russia’s export restrictions over time, as well as details about its most recent policy.

- “Global Food Price and Policy Outlook” in Wheat Outlook: December 2021: This article provides a view of global food price inflation statistics. The report considers price metrics for different categories of food as well as country-specific data. The article also details a few of the trade measures that have been taken by some countries to lessen the impacts of high commodity prices in the current environment.

- “The Effect of Rising Wheat Prices on U.S. Retail Food Prices” in Wheat Outlook: November 2021: This article discusses the trends in U.S. wheat prices as well as the trends in prices of wheat-based food products. The report notes that the prices of wheat grain tend to be more volatile, while changes in wheat product pricing is relatively stable over time.

- Merits of an Aggregate Futures Price Forecasting Model for the All Wheat U.S. Season-Average Farm Price: This report presents an alternative, aggregate futures-based forecasting model that uses the three available wheat futures contract prices, which represent the majority of U.S. wheat production. Results show that this model tends to provide forecasts with a lower mean absolute percent error and a more accurate prediction of positive directional movement (April 2021).

- “An Overview of the Locust Outbreak in Africa and Implications for 2020/21 Wheat Supplies” in Wheat Outlook: August 2020: This report discusses the effects of locust outbreaks on crop production in several East African countries. Overall, the report notes that wheat production in these countries is not expected to be significantly affected by the outbreaks, partly because the largest swarms are located away from the major wheat production areas. Even when the amount of national crop production is down due to the presence of locusts, there are often other factors contributing to crop losses (August 2020, page 13 of PDF).

- “Brazil’s Implementation of a TRQ for Wheat Cracks Open the Door for Expanded U.S. Exports” in Wheat Outlook: December 2019: This report analyzes the expected competitiveness of U.S. wheat exports to Brazil after the opening of Brazil’s Wheat tariff-rate quota (TRQ) (December 2019, page 6 of PDF).

- “Replacement Agreement for NAFTA to Require Reciprocal Grading Standards for Wheat” in Wheat Outlook: October 2018: This report provides background on the regulatory changes proposed in the United States-Canada-Mexico Agreement requiring reciprocal grading standards for wheat among the member countries (October 2018, page 7 of PDF).

- “Major Changes in Russian and Ukrainian Crop Area During Economic Transition” in Wheat Outlook: May 2018: This report discusses structural changes in the agricultural sectors for Russia and Ukraine, with particular emphasis on the shifting of area between different commodities (May 2018, page 11 of PDF).

- “Prospects for Russian Wheat Yields and Yield Volatility” in Wheat Outlook: January 2018: This report discusses the background for the rising trend in Russian wheat yields. The report further provides a comparison of winter and spring yields, as well as yield comparisons to other major world producers (January 2018, page 7 of PDF).

- Wheat Price Discovery Remains Concentrated in the United States, but is Shifting to Europe: This report discusses the general trend in the wheat futures market utilization between the United States (Chicago) and Europe (Paris). Futures markets in the United States are noted as being the most used for wheat market price discovery, but the trend is shifting toward Europe, as more of the world’s exports are represented by that region (October 2017).

- Productivity Growth and the Revival of Russian Agriculture: Russia's agricultural total factor productivity in 1994–2013 reveals that output specialization has been a key feature of agricultural recovery in the transition to a market economy. Some districts specialized more in grains and oilseeds, others in animal products. The fastest productivity growth occurred in the South, which emerged as Russia's most important agricultural district (April 2017).

- Changing Crop Area in the Former Soviet Union Region: This 2017 report examines how total crop area and area for grain changed in Russia, Ukraine, and Kazakhstan. After falling substantially in all three countries during the 1990s, total area and grain area rebounded somewhat in Ukraine and Kazakhstan, but currently, area is still far below the levels of the late Soviet period in Russia and Kazakhstan (February 2017).

- Global Macroeconomic Developments Drive Downturn in U.S. Agricultural Exports: The macroeconomic outlook underlying the 2016 USDA 10-year agricultural projections indicates slower global income growth, particularly in developing countries, and a stronger dollar. This shift in the macroeconomic environment relative to the past decade implies smaller projected increases in agricultural trade and declines in U.S. market share relative to previous projections (July 2016).

- Thinning Markets in U.S. Agriculture: As markets have fewer purchases, low trading volume, and low liquidity, U.S. agriculture is growing more concentrated, which raises concerns about equity for producers and efficiency in market performance (March 2016).

- Deconstructing Wheat Price Spikes: A Model of Supply and Demand, Financial Speculation, and Commodity Price Comovement: In 2008, wheat futures prices spiked and then crashed along with prices for other agricultural and nonagricultural commodities. This study uses an econometric model to explain the influence of various factors, including passive speculation by large traders, on wheat prices. Findings show that market-specific changes related to supply and demand for wheat were the dominant cause of price spikes (April 2014).

- Recent Convergence Performance of Futures and Cash Prices for Corn, Soybeans, and Wheat: From 2005 to 2011, wheat, corn, and soybean futures contracts were affected by growing discrepancies between expiring futures prices and cash prices—a problem known as non-convergence. In response, the futures exchanges modified their contracts to better reflect market conditions. Those modifications appear to have improved convergence in these markets since 2011 (December 2013).