U.S. wholesale beet and cane sugar prices return to more similar levels in 2016/17

- by Michael J. McConnell

- 1/18/2018

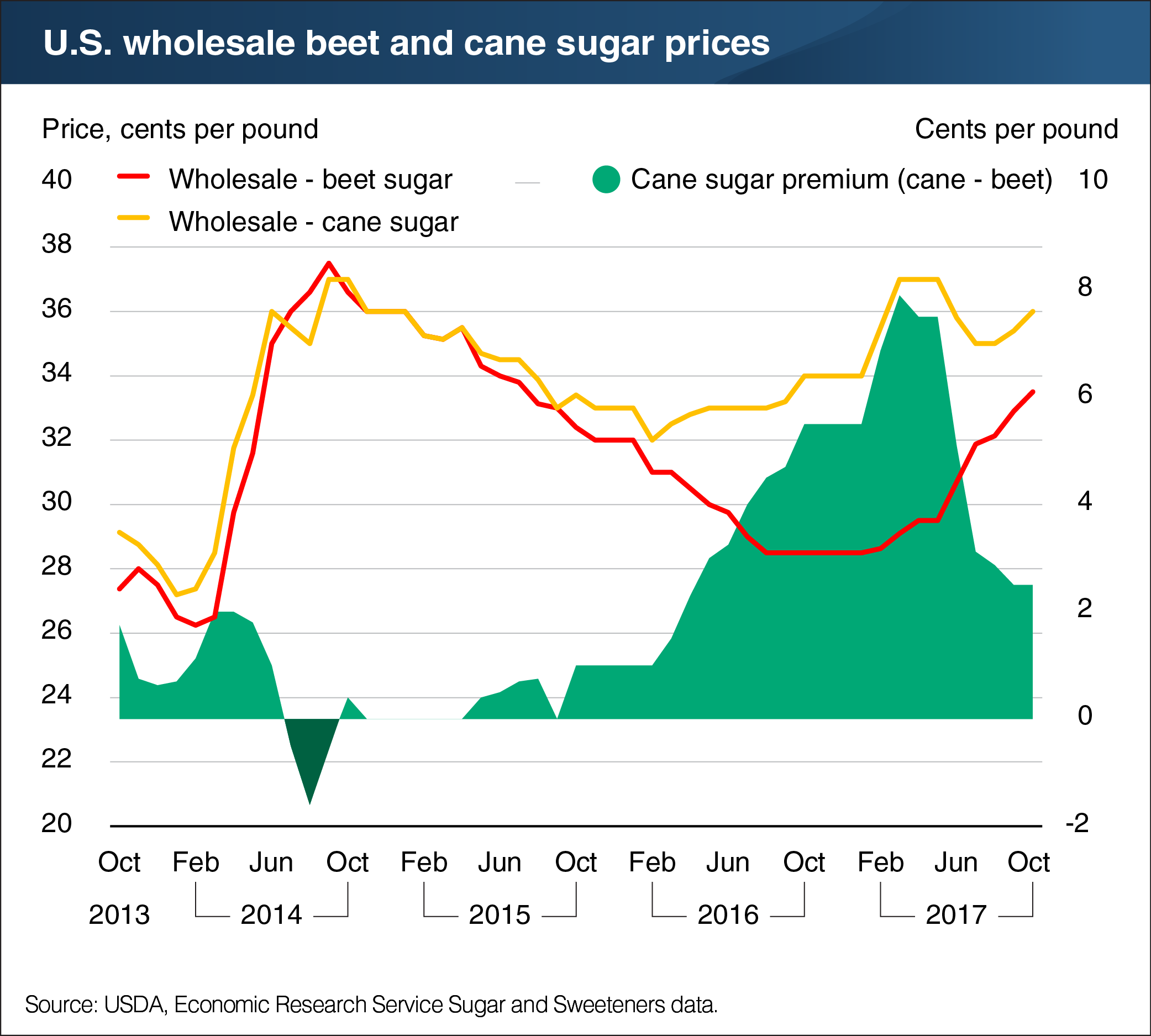

One of the major developments in the U.S. sugar market during the 2016/17 marketing year occurred when the beet and cane sugar sectors returned to the levels of the broader market. Ending stocks for cane and beet sugars diverged significantly in 2015/16, with extremely tight cane sugar supplies and ample beet sugar inventories. This resulted in large price differences in refined cane and beet sugars. The price differential also played an important role in reconciling the divergences in the cane and beet sugar sectors. Wholesale spot prices of refined cane sugar began the year at a 5.5-cent per pound premium to refined beet sugar. That premium grew to nearly 8 cents by March before narrowing to 2.5 cents by the end of the year. With demand for sugar continuing to grow steadily, the relative beet sugar price discount was one of the key market drivers that spurred the large beet sugar deliveries and drew down inventories. While the price differential narrowed, refined cane sugar prices finished the year higher than they started, reflecting both the constrained supplies in the cane sugar sector and the broader U.S. refined sugar market. This chart is drawn from the special article Beet and Cane Sugar Inventories Return to Comparable Levels After Divergence in 2015/16, published in the November ERS Sugar and Sweeteners Outlooknewsletter.