Impact of changing capital gains taxation at death varies by farm size

- by Tia M. McDonald, Ron Durst and Christine Whitt

- 10/6/2021

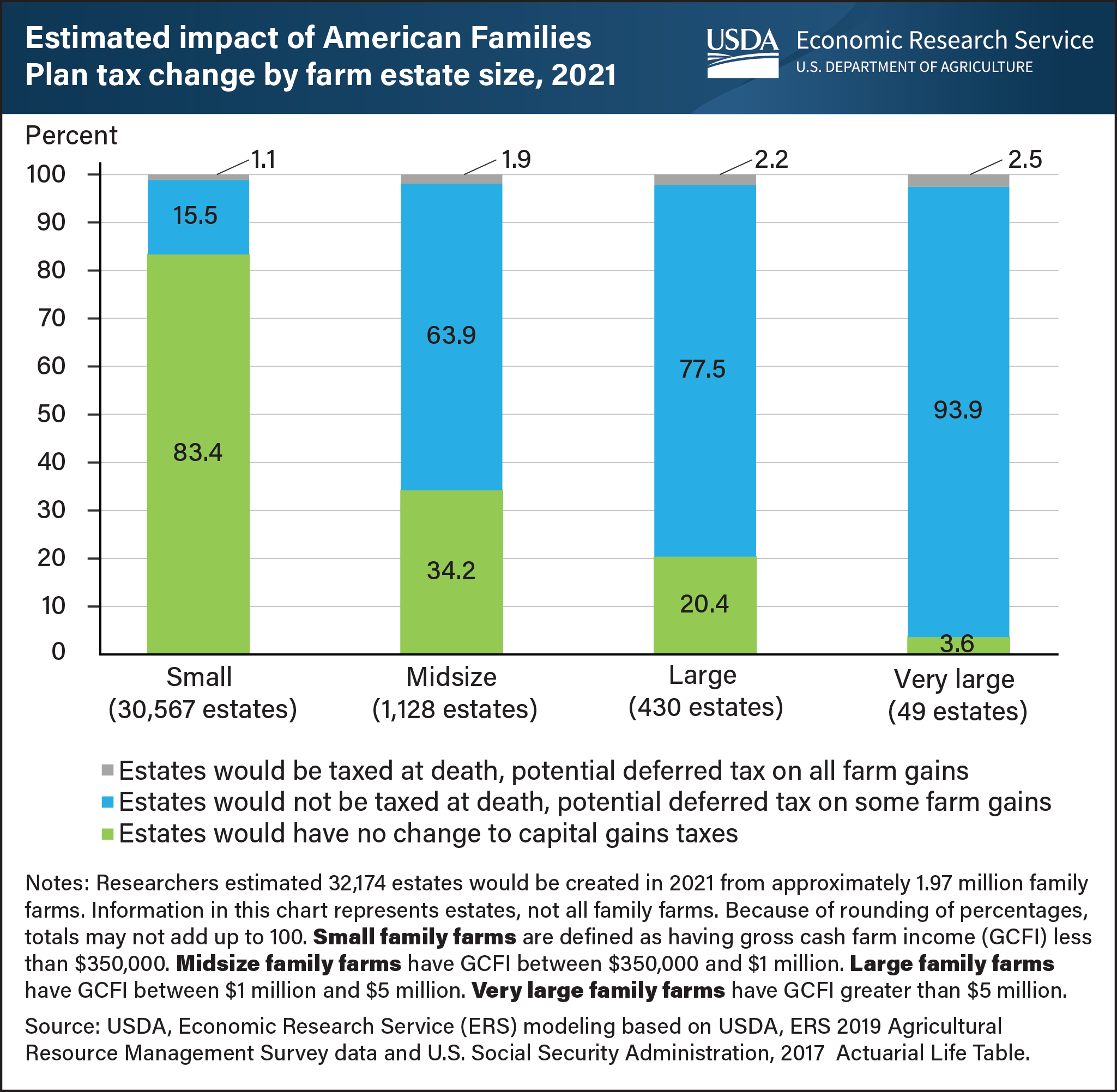

A proposal to change the way capital gains are taxed at death would affect family farm estates differently according to the size of the farm. Under current law, most inherited assets receive a step-up in basis, which means the tax basis—the amount for determining gain or loss—of property transferred to an heir at death is increased to its current fair market value at the date of death, eliminating any capital gains tax liability on those inherited gains. The change, which was included in the American Families Plan (AFP), would end stepped-up basis for gains above $1 million for the estates of individuals or $2 million for married couples. Gains above these exemption amounts would be subject to tax at death. However, the transfer of a family farm to a family member who continues the operation would not result in a tax at death. Farm and business assets exceeding the exemption amounts would receive a carry-over basis deferring capital gains tax until the assets are sold, or until the farm is no longer family owned and operated. USDA, Economic Research Service (ERS) researchers, using modeling to evaluate potential effects of the AFP proposal, found that as family farm size increased, the estimated share of estates owing no tax at death and receiving stepped-up basis on all assets decreased, while the estimated share of estates that would receive carry-over basis increased. For small farm estates, with gross cash farm income (GCFI) less than $350,000, 83.4 percent would owe no capital gains tax at death and would receive a stepped-up basis on all assets, resulting in no change to their capital gains tax liability. Under the ERS model, that share would drop to 34.2 percent for midsize farms (those with GCFI of $350,000 to $1 million), 20.4 percent for large farms (with GCFI of $1 million to $5 million), and 3.6 percent for very large farms (with GCFI of more than $5 million). Some estates would be taxed on nonfarm gains at death and potentially could owe deferred taxes on farm gains if the heirs stop operating the farm. For those estates, the estimated share increased from 1.1 percent for small farms to 2.5 percent for very large farms. Other estates would not have to pay tax at death but could see deferred taxes on farm gains if the heirs stop operating the farm. For that group, the estimated share increased from 15.5 percent for small farms to 93.9 percent for very large farms. This chart can be found in the ERS report The Effect on Family Farms of Changing Capital Gains Taxation at Death, published September 2021.