How proposed capital gains tax changes could affect estates of family farms

- by Tia M. McDonald, Ron Durst and Christine Whitt

- 9/22/2021

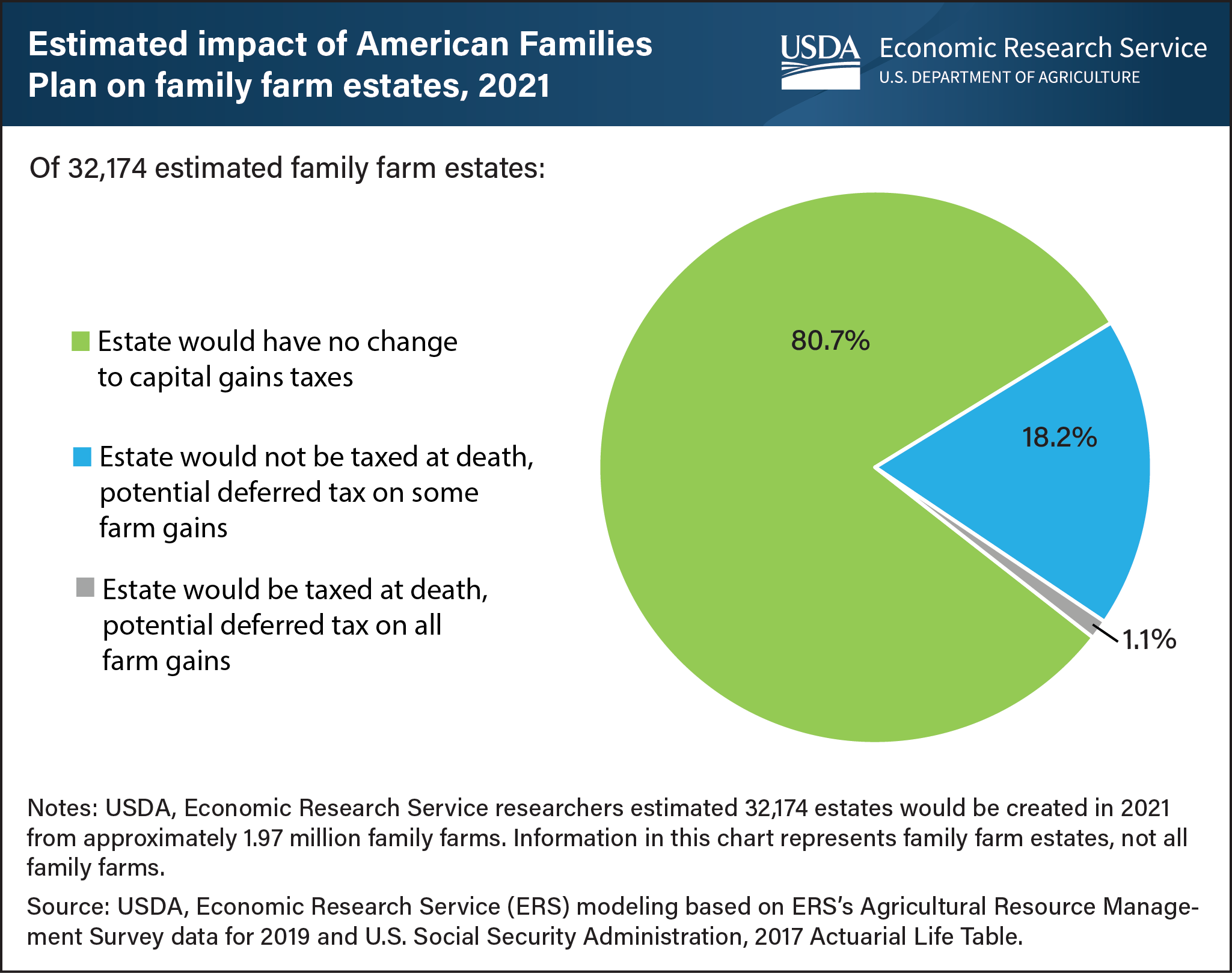

The American Families Plan (AFP) that President Joe Biden announced in April 2021 included a proposal to make accumulated gains in asset value subject to capital gains taxation when the asset owner dies. Under current law, asset value gains can be passed on to heirs without being subject to capital gains taxation because the value of the assets are reset to the fair market value at the time of inheritance. This adjustment in asset valuation, known as a “stepped-up basis,” eliminates capital gains tax liabilities on any gains incurred before the assets were transferred to the heirs. AFP also included a provision that would exempt from capital gains taxes $1 million in gains for the estates of individuals and $2 million in gains for the estates of married couples, as well as for gains on a personal residence of $250,000 for individuals and $500,000 for married couples. Gains above these exemption amounts would be subject to tax at death. However, the transfer of a family farm to a family member who continues the operation would not result in a tax upon the death of the principal operator. Under the proposal, any remaining farm and business gains above the exemption amount would receive a “carry-over basis” that effectively defers any capital gains tax until the assets are sold or until the farm is no longer family-owned and operated. Using 2019 Agricultural Resource Management Survey data, USDA, Economic Research Service (ERS) researchers estimated that of the 1.97 million family farms in the United States, 32,174 estates would result from principal operator deaths in 2021. From these farm estates, the ERS model used to evaluate potential effects of the AFP proposal estimated that heirs of 80.7 percent of family farm estates would have no change to their capital gains tax liability upon death of the principal operator. Heirs of 18.2 percent of family farm estates would not owe taxes at the time of the principal operator’s death but could be subject to a future potential capital gains tax obligation on inherited farm gains if the heirs stop farming. Heirs of 1.1 percent of estates would owe tax on nonfarm gains upon death of the principal operator and have a future potential capital gains tax obligation resulting from inherited farm gains if the heirs stop farming. This chart can be found in the ERS report The Effect on Family Farms of Changing Capital Gains Taxation at Death, published September 2021.