Self-Employed Workers Are Less Likely To Have Health Insurance Than Those Employed by Private Firms, Governments

- by Elizabeth A. Dobis and Jessica E. Todd

- 7/5/2022

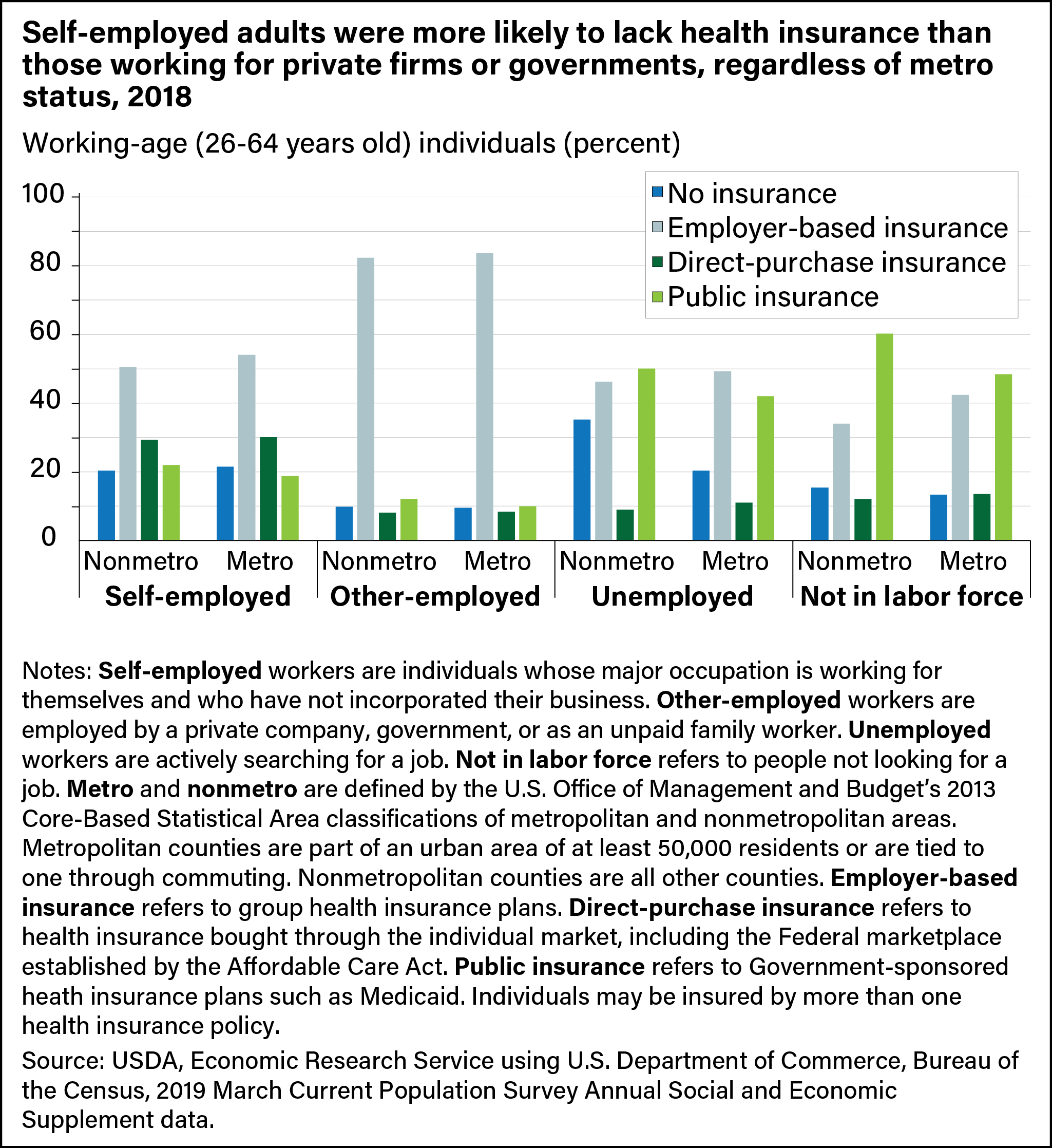

In 2018, health insurance coverage rates and patterns in metropolitan (metro) and nonmetropolitan (nonmetro) areas were similar, according to research by the USDA, Economic Research Service (ERS). That year, 88.9 percent of working-age adults (aged 26–64) in metro counties and 87.5 percent of those in nonmetro counties had health insurance coverage. The source of employment had a greater effect on health insurance coverage than whether a worker lived in a nonmetro or metro county. In 2018, self-employed working-age adults were less likely to have health insurance coverage than those employed by private firms or governments, no matter where they lived (metropolitan or nonmetropolitan area). As a result, they may have found it difficult to access health care, as affordability often is tied to health insurance coverage.

In March 2019, a sample of U.S. residents were surveyed about their health insurance coverage in the previous calendar year. Based on that survey, nationally, 4.5 percent of working-age adults were self-employed, meaning they worked for themselves as their primary occupation and had not incorporated their businesses. In nonmetro counties, 5.8 percent of working-age adults were self-employed, compared with 4.3 percent in metro counties. A smaller share of nonmetro self-employed workers was uninsured than metro self-employed workers (20.4 percent versus 21.5 percent) in 2018. So, while nonmetropolitan counties have a higher portion of self-employed workers than metropolitan counties, nonmetro counties have a slightly lower proportion of uninsured self-employed workers. At the same time, employees in private or government jobs in nonmetro counties were uninsured at less than half the self-employed rate at 9.8 percent. Unemployed working-age adults in nonmetro areas had the highest uninsured rate at 35.2 percent.

With less access to employer-sponsored group health insurance plans, self-employed workers could buy a plan directly from an insurance company or through the Federal health insurance marketplace established by the Affordable Care Act. They also could obtain coverage from a publicly subsidized plan such as Medicaid or from a family member’s employer-based plan.

Of self-employed working-age nonmetro residents with health insurance, 50.5 percent were covered by employer-based plans, often through a family member’s plan. Among nonmetro households with a mix of self-employed and other-employed workers, 58.5 percent of the self-employed workers were dependents of household members who had an employer-based plan. Self-employed workers with employer-based health insurance coverage also may have joined a group plan through a social organization or have a plan from another job (besides their primary self-employment).

In nonmetro counties, a greater share of self-employed working-age adults (29.3 percent) were covered by direct-purchase health insurance plans than those who worked for others, were unemployed, or were outside the labor force. Families with direct-purchase plans paid more per person in insurance premiums in 2018 than families with other sources of health insurance coverage. Nearly twice the percentage of nonmetro self-employed workers were insured through public plans such as Medicaid than those employed through private firms or governments (22.0 percent versus 12.1 percent). Families covered by public health insurance plans paid the least in premiums per person.

This article is drawn from:

- Dobis, E.A. & Todd, J.E. (2022). Health Care Access Among Self-Employed Workers in Nonmetropolitan Counties. U.S. Department of Agriculture, Economic Research Service. AP-099.

You may also like:

- Whitt, C. & Todd, J.E. (2020, March 2). Family Farm Households Reap Benefits in Working Off the Farm. Amber Waves, U.S. Department of Agriculture, Economic Research Service.

- Dobis, E.A. & McGranahan, D. (2021, February 1). Rural Residents Appear to be More Vulnerable to Serious Infection or Death From Coronavirus COVID-19. Amber Waves, U.S. Department of Agriculture, Economic Research Service.

- Farm Household Well-being. (n.d.). U.S. Department of Agriculture, Economic Research Service.