Rural Businesses That Receive USDA Business and Industry Guaranteed Loans Less Likely To Fail

- by Anil Rupasingha and John Pender

- 9/3/2019

The success of rural small businesses depends on access to readily available capital. USDA implements several loan and grant programs to support rural businesses. Of these, the Business and Industry (B&I) Guaranteed Loan Program is the largest, with a program level of $892 million (the total value of all loans given under the program) in 2017. The goals of the program are to save and create new jobs and to stimulate rural economies. The B&I program provides guaranteed loans in rural areas in partnership with private-sector lenders. By reducing lenders’ risk, the program encourages them to provide more generous terms or larger principal amounts, or to approve loans to rural businesses that they otherwise would not make.

To understand the effects of the B&I program on recipient businesses, ERS researchers conducted a study comparing the survival of businesses that received B&I loans with the survival of similar businesses that never had B&I loans. The study estimated business survival rates between 1990 and 2013 for B&I loan recipients and a comparison group of non-recipients similar to loan recipients based on several key factors that affect business survival, including business location, industry, age, and employment size. The analysis excluded startup businesses with no employment history because the number of employees prior to receipt of a B&I loan was needed to identify the comparison group. On average, B&I recipients and the group of similar non-recipients had about 12 employees, and B&I recipient businesses were about 6 years old at the time of receiving a B&I loan.

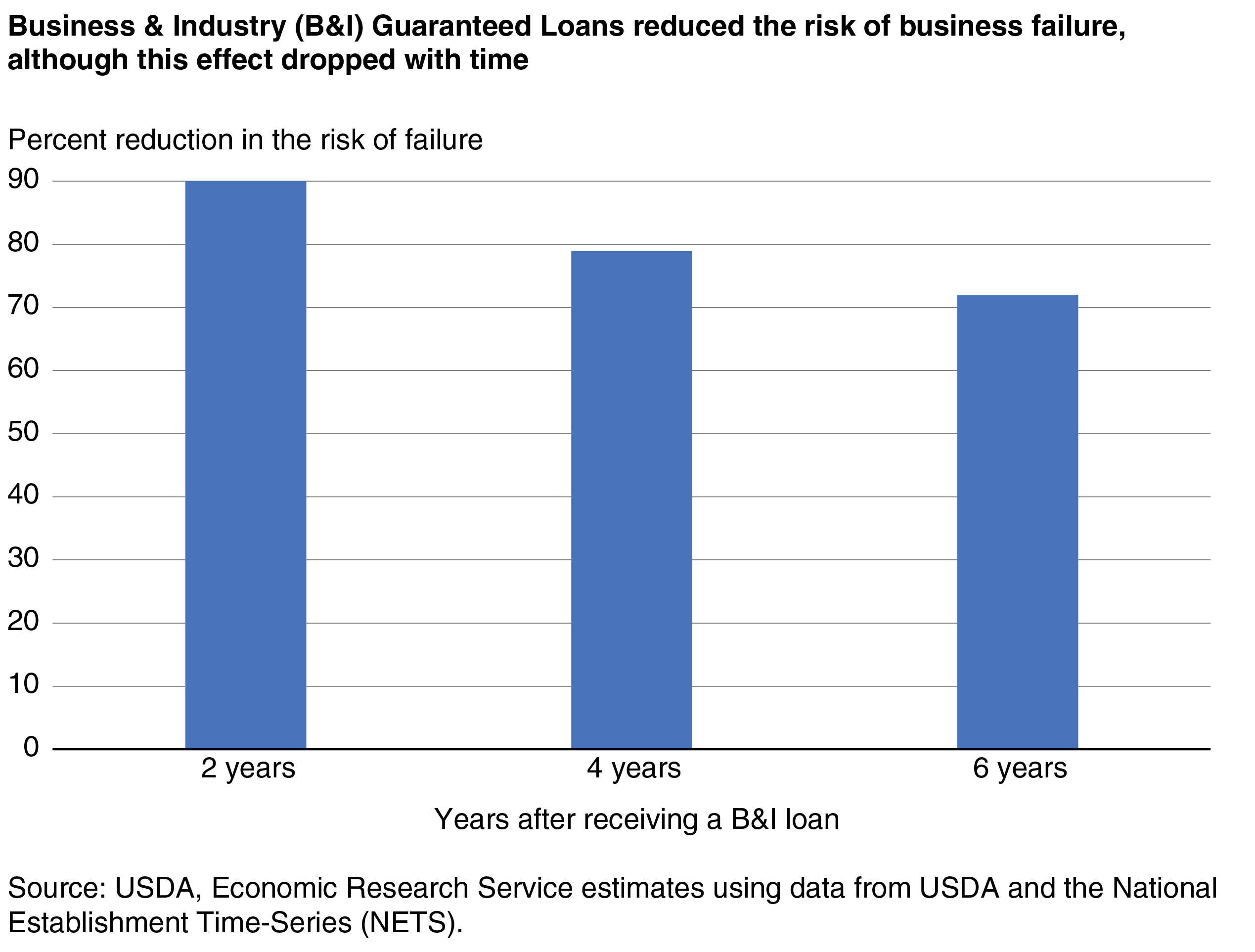

ERS researchers estimated the effect of receiving a B&I loan on the survival of businesses at different periods of time after receipt of the loan: 2 years, 4 years, and 6 years after the loan. Findings show that, on average, 2 years after receiving a B&I loan, recipients were 90 percent less likely to fail in the next year than the group of similar non-recipients. The predicted likelihood of failure within the next year for B&I loan recipients 2 years after receiving a loan was about 0.30 businesses out of 1,000 B&I loan recipient businesses. This compared to a failure rate of approximately 3 per 1,000 non-recipient businesses sharing the same age and other characteristics.

The effect of B&I loans on survival rates declined with time. Nevertheless, 4 years after receiving a B&I loan, recipients were still 79 percent less likely to fail in the next year than similar non-recipients. And 6 years after receiving a B&I loan, recipients were 72 percent less likely to fail in the next year than similar non-recipients. The B&I Loan Program’s strong effects on business survival suggest that the program has helped retain existing jobs in local communities.

This article is drawn from:

- Rural Business Programs and Business Performance: The Impact of the USDA’s Business and Industry (B&I) Guaranteed Loan Program, by Anil Rupasingha, Daniel Crown (The Ohio State University), and John Pender. (2018). Journal of Regional Science, pp. 1-22, https://doi.org/10.1111/jors.12421.

You may also like:

- Rupasingha, A., Pender, J. & Wiggins, S. (2018). USDA’s Value-Added Producer Grant Program and Its Effect on Business Survival and Growth. U.S. Department of Agriculture, Economic Research Service. ERR-248.