Federal Crop Insurance Is Associated With Higher Levels of Short-Term Farm Debt

- by Jennifer Ifft, Todd Kuethe and Mitch Morehart

- 10/5/2015

Federal crop insurance (FCI) has become a key component of U.S. farm policy. FCI provides farmers with subsidized insurance against unanticipated declines in market prices or yields. The availability of such insurance may affect farmer decisions about other risk management strategies.

Like many farm programs, FCI has been implemented at the national level; participation is available to most farms and is voluntary. A farmer’s decision about whether to purchase crop insurance is likely to be based on the same factors that determine the farm’s debt level, since both decisions involve choices about risk. An ERS study analyzed the relationship between debt use and FCI participation by farm businesses. Researchers first estimated the difference in debt use between similar farm operations with and without FCI coverage and then used other statistical techniques to model how decisions about farm debt and crop insurance participation are jointly determined.

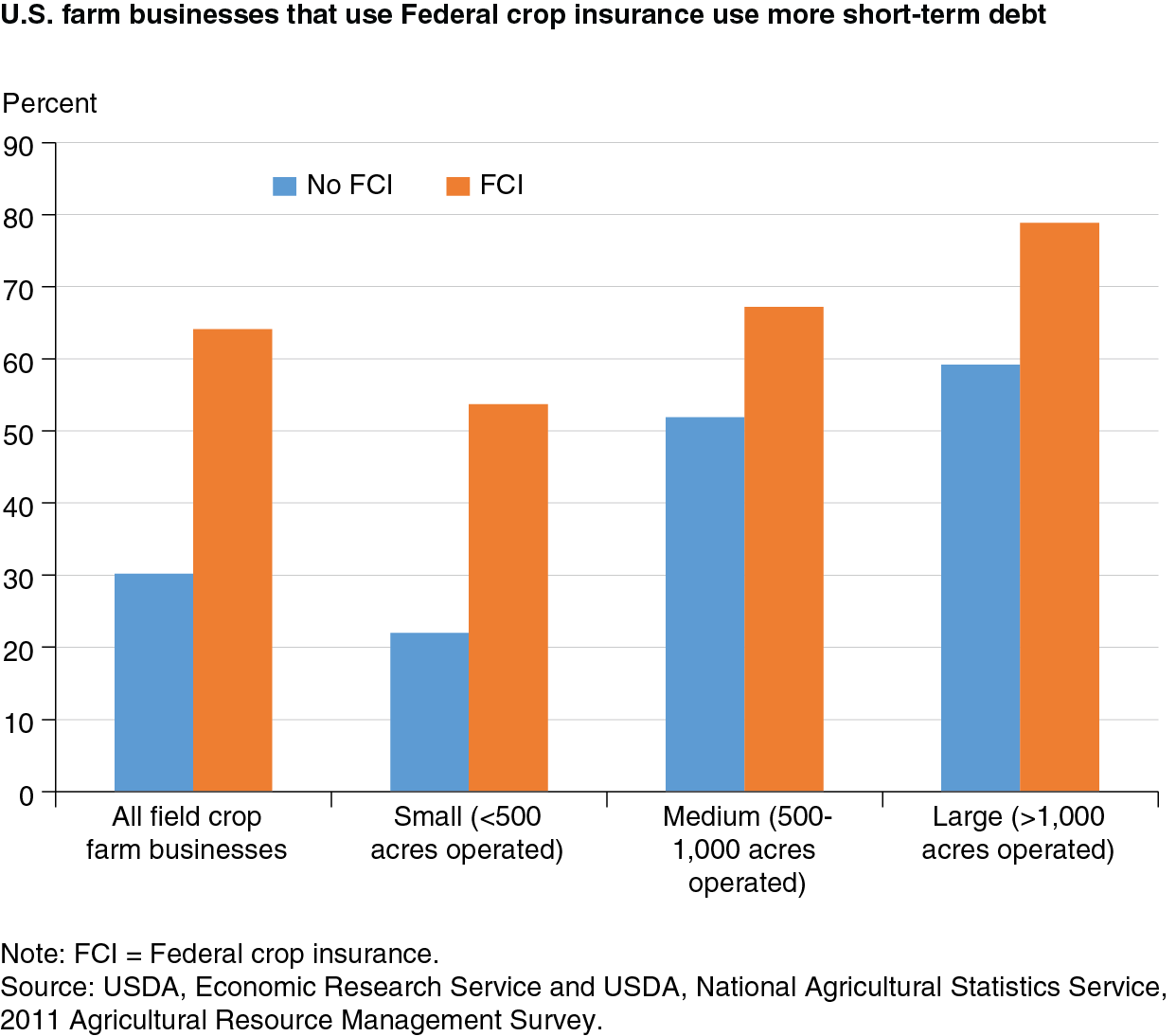

U.S. farm businesses that use Federal crop insurance use more short-term debt (or operating loans) than farms without insurance. This behavior is consistent with risk balancing, and this pattern holds even after accounting for other farm characteristics. The analyses done by ERS make it possible to compare debt levels between similar farms with and without Federal crop insurance coverage. An example of the results for farm businesses specializing in field crops in 2011 illustrates the strength of the relationship between short-term debt and insurance use. The ratio of production loans to variable expenses is twice as high for field crop farm businesses that use FCI; use of short-term loans is also higher. However, higher levels of long-term debt are generally not associated with FCI participation.

These findings may be related to the growing use of short-term debt to cover increasing farm production expenses. Agricultural lending standards are generally conservative (set to minimize risk to the lender), and the farm sector as a whole currently has a historically low debt-to-asset ratio. Taken together, these considerations suggest that the increase in average debt use in response to FCI may not be a threat to the financial health of the farm sector. However, if one of the goals of the FCI program is to lower the risk faced by farm operations, these results suggest that the net reduction in total risk facing the farm sector due to FCI may be less than the decline in risk provided directly by FCI.

This article is drawn from:

- “Does Federal Crop Insurance Lead to Higher Farm Debt Use? Evidence From the Agricultural Resource Management Survey,” by Jennifer Ifft, Todd Kuethe, and Mitch Morehart. (2015). Agricultural Finance Review.