China’s Cotton Policies To Lower Domestic Consumption and Imports

- by James Kiawu

- 4/1/2013

China’s recent changes in cotton policies have implications for world consumption and trade in cotton. In 2011, China announced a minimum support price for cotton, defended by a program of government purchases and stockholding. The resulting large procurements of domestic cotton raised local prices above world market levels. In 2012, China increased the minimum support price, even as world cotton prices were declining, causing a 50- to 70-percent price premium for domestic cotton. These policy changes have severely constrained the profitability of cotton spinning in China and are expected to lower China’s cotton consumption and import demand, while boosting imports and mill use by other countries.

China’s shift in cotton policy followed the 2010 global price shocks, which resulted in record-high world cotton prices. To stabilize prices and ensure cotton availability to domestic spinners, China depleted its reserve stocks in 2010 and, in the following year, offered a generous price incentive to its farmers. The rationale was to offset any potential decline in output as global cotton prices retreated from the 2010/11 spike. These initiatives replenished China’s reserve stocks by an additional 18 million bales, equivalent to 45 percent of the 2011/12 domestic crop.

Historically, China’s agricultural policies heavily favored the production of grain, especially rice, over cotton. Since 2004, grain producers have enjoyed floor prices, production subsidies, and direct payments aimed at alleviating the gap between rural and urban incomes and bolstering food security. At the same time, cotton production was constrained by rising wages, labor shortages, and the slow pace of mechanization. The recent changes in cotton policy were an attempt to offset some of these cotton production constraints, expand the government’s efforts to narrow the gap between rural and urban incomes, and reduce the disparity between cotton and rice support.

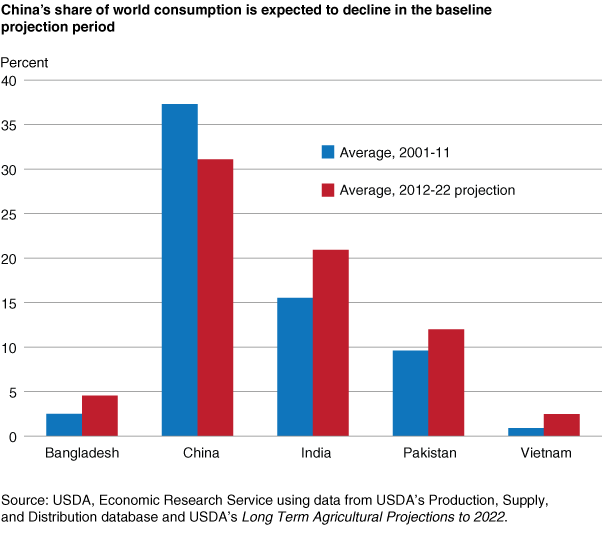

China’s ranking as the world’s leading producer, consumer, and importer of cotton is not expected to change in the foreseeable future. The recent policy changes, however, are expected to elevate domestic prices, lower mill use, and reduce profits to spinners. When China eventually offloads some of the national reserve stocks on the world market, the subsequent price decline is expected to have negative implications for U.S. cotton growers and exporters. China--a net cotton importer--is projected to lose global import and mill use shares to other countries. According to USDA’s 2013 long-term projections, China’s imports are projected to decline in the next decade, while imports by Bangladesh, Pakistan, and Vietnam are projected to increase.

This article is drawn from:

- Cotton and Wool. (n.d.). U.S. Department of Agriculture, Economic Research Service.

- Westcott, P. & Trostle, R. (2013). USDA Agricultural Projections to 2022. U.S. Department of Agriculture, Economic Research Service. OCE-131.