North American Greenhouse Tomatoes Emerge as a Major Market Force

- by Linda Calvin and Roberta Cook

- 4/1/2005

The rapidly growing greenhouse tomato industry has become an important part of the North American fresh tomato industry. Greenhouse tomatoes now represent an estimated 17 percent of U.S. fresh tomato supply. Even though greenhouse tomatoes still constitute a minority share of the U.S. fresh tomato market, their influence is concentrated and growing in retail channels, which represent about half of U.S. tomato consumption. Around 37 percent of all fresh tomatoes sold in U.S. retail stores are now greenhouse, compared with negligible amounts in the early 1990s.

Greenhouse tomatoes can be seen as just one more development in a trend toward more differentiated fresh tomato offerings, including more variety in field-grown tomatoes. New types of tomatoes, improved varieties and handling, and positive health benefits associated with eating tomatoes have all contributed to a 30-percent rise in U.S. consumption of fresh tomatoes since 1985, with estimated 2003 annual per capita consumption levels around 8.8 kilograms (19.4 pounds). Growth in the greenhouse industry has challenged growers of fresh field tomatoes. With rising consumption of all tomatoes, field tomato sales in the U.S. retail market increased through 2001, in part due to new fresh field products, such as grape tomatoes. But in 2002, the combined retail sales volume of all field tomato types began to slip. Field tomatoes still dominate the growing foodservice market (restaurants, schools, hospitals, etc.) where greenhouse tomatoes are scarce. Foodservice sales are increasingly essential to the health of the field tomato industry.

While greenhouse tomatoes have higher per unit costs of production and generally higher retail prices than field tomatoes, several other characteristics have contributed to the growth in this sector. Since they are protected from weather and other conditions affecting open field production, greenhouse tomatoes generally have a much more uniform appearance than field tomatoes. They are also less prone to swings in production volumes. These factors lead to greater consistency in quality, volumes, and pricing—issues of particular concern to the retail and foodservice industries.

The United States, Canada, and Mexico have all developed major greenhouse industries. The United States is the largest North American market for greenhouse tomatoes, and U.S. imports from Canada and Mexico are larger than domestic production. In recent years, the growth in U.S. imports has exceeded the growth in U.S. production. In 2003, Canada accounted for an estimated 46 percent of U.S. imports of greenhouse tomatoes. Mexico’s share was 45 percent. As the greenhouse tomato industry has transitioned from niche to mainstream status, it has become part of a more integrated North American market, following the pattern established by the field tomato industry.

The greenhouse industry is facing growing pains. With rapid growth in Canada and the United States during the 1990s, greenhouse tomato prices declined, causing financial problems for some growers. More recently, as the industry has expanded in Mexico, heterogeneity in production methods has increased. Growers in the United States and Canada, and some Mexican growers, have high-technology and high-cost greenhouses. Many of these growers view the growth of lower technology greenhouses and shade houses in Mexico with some alarm. This has led to a debate in the industry about how to define a greenhouse tomato (see “What Is a Greenhouse Tomato?”). Regardless of how this issue is resolved, higher expected year-round production volumes in Mexico portend greater competition in all seasons, and continued downward pressure on prices.

Seasonality Drives Market Integration

Seasonality is a major factor shaping the North American fresh tomato industry. Consumers increasingly demand a steady year-round supply of an ever-greater variety of tomato products. The greenhouse industry has seasonal production patterns similar to the fresh field industry, despite the fact that greenhouse production takes place indoors. Greenhouse supplies vary over time and across geographical regions, and marketers often try to extend their seasons to periods typically marked by lower tomato production and higher prices, sometimes by sourcing from more than one location. The result has been the development of an integrated North American greenhouse tomato industry that can provide the variety of tomato products that consumers demand throughout the year. While there is some overlap, Mexico is the primary foreign winter supplier to the U.S. market and Canada the primary foreign summer supplier.

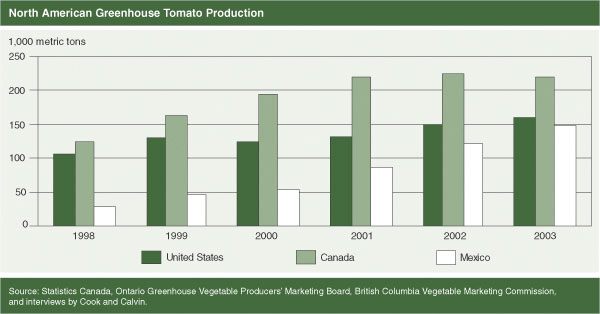

In 2003, total production of North American greenhouse tomatoes was estimated at 528,078 metric tons. Canada’s share of this total was 42 percent, followed by the United States with 30 percent, and Mexico with 28 percent. Though greenhouse tomato production soared in all three countries from the early 1990s, it has been stabilizing in the United States and Canada. In Mexico, the industry is still growing rapidly. Mexico’s growing area exceeds the combined total area of U.S. and Canadian greenhouses, but with many Mexican growers using extensive production methods with relatively simple low-yielding technology, output is lower than in the other two countries.

Canada was the first big greenhouse tomato producer in North America and still has the highest yields and total production. The Canadian industry is centered in southern British Columbia and Ontario. Long, relatively mild, summer days in these regions generate high yields. During the March to December period, Canadian production is a market force. U.S. and Mexican tomato producers, both field and greenhouse, have to compete with the high Canadian summer volume.

The Achilles heel of the Canadian greenhouse tomato industry is its lack of winter supply. As greenhouse tomatoes have become a mainline commodity, retailers are increasingly demanding consistent year-round volumes from their suppliers. Given current greenhouse prices, it is uneconomical for most Canadian producers to provide light and heat for winter production. To better serve their customers, Canadian marketers supplement their winter supply by sourcing from U.S. and Mexican producers. But this pattern could change. More Mexican producers may become year-round suppliers and decide to market their tomatoes independently. Foreign direct investment in growing operations could become more common as a strategy for controlling supply. For example, one large British Columbia grower built a greenhouse in California to help supplement winter supplies.

| Production category | United States | Canada | Mexico | North America |

|---|---|---|---|---|

| Greenhouse tomato production (1,000 metric tons) | 160 | 220 | 148 | 528 |

| Greenhouse tomato area (hectares) | 330 | 446 | 950 | 1,726 |

| Average greenhouse tomato yield (metric tons/hectare) | 484 | 494 | 156 | 378 |

| Fresh field tomato production, excluding processing (1,000 metric tons) | 1,594 | 27 | 1,804 | 3,425 |

| Average fresh field tomato yield (metric tons/hectare) | 32 | 15 | 28 | 25 |

| Greenhouse share of total fresh production, by country (percent) | 9 | 89 | 8 | 13 |

| Estimated greenhouse exports to U.S. (1,000 metric tons) 1 | N/A | 130 | 126 | 256 |

| 1Official imports of greenhouse tomatoes are thought to be underreported for Mexico due to tariff code misclassification; 58,357 metric tons of greenhouse tomato imports from Mexico were reported by the U.S. Department of Commerce in 2003. The figure shown here includes estimated additional miscoded imports, based on information from industry sources obtained by Cook and Calvin. This figure may include some production from shade houses. N/A = Not applicable. Sources: Statistics Canada, Ontario Greenhouse Vegetable Producers’ Marketing Board, British Columbia Vegetable Marketing Commission, U.S. Department of Commerce, interviews by Cook and Calvin, USDA’s National Agricultural Statistics Service, USDA’s Foreign Agricultural Service. |

||||

Much of the U.S. greenhouse tomato industry began in the northeast in the early 1990s, with production in the same months as Canadian producers. Eventually, several producers moved west and south, lured by the prospect of producing tomatoes year-round and capturing a slice of the high-priced winter market. The four largest greenhouse tomato firms in the United States are now located in Arizona, Texas, Colorado, and coastal southern California, and account for 67 percent of domestic production. Smaller greenhouses are located throughout the United States but these are frequently seasonal producers and local marketers. The profitable winter market helps the year-round U.S. producers withstand the very low prices during the summer season when Canadian volume inflates supplies. However, southwestern greenhouses face special challenges posed by the summer heat and often need expensive cooling systems to produce high-quality tomatoes. Furthermore, expanding winter production in Mexico will likely reduce greenhouse tomato prices and increase competitive pressure on year-round U.S. growers.

The Mexican greenhouse tomato industry is the fastest growing in North America and the most varied. In Mexico, large field tomato grower-exporters in Sinaloa on the northwest coast and the Baja California peninsula are experimenting with protected culture, either shade houses or greenhouses, near their field operations. In contrast, U.S. field tomato growers usually have no connections to the greenhouse industry. This gives Mexican growers a foot in both camps and potentially reduces market and other types of risk. Because of its hot, humid summers, Sinaloa, the principal fresh field tomato-exporting region in Mexico and a leading greenhouse exporter, is a winter producer only. Growers there have less incentive to invest in the highest technology greenhouses because the limited shipping season reduces the return on investment. Nevertheless, the technology levels and yields in coastal areas are improving, with more growers moving into midlevel technology systems to improve yields, quality, and marketing.

Several clusters of greenhouses are also emerging in temperate, higher altitude areas in central and north central Mexico, and in Imuris in northern Sonora, near the U.S. border. With the exception of those in Imuris, most of these firms are new entrants to agriculture and have no connection with field tomato growers. Their advantage is the ability to produce year-round, in some cases with investment in summer cooling required. As a result, more growers in these areas are investing in high-technology greenhouses similar to those in Canada and the United States. As greenhouse production in temperate, noncoastal areas expands, Mexico will become more of a competitive force in all seasons.

The Mexican greenhouse tomato industry has both advantages and disadvantages over the U.S. and Canadian industries. Mexico’s major advantage is its ability to produce during the winter months—the same edge it holds in field tomato production. Its major disadvantage is the much higher cost of capital, a problem given the capital-intensive nature of greenhouse production. As a result, many growers find it difficult to invest in technologies that generate the best yields and consistent quality. Mexico is also hampered by lack of local greenhouse input industries, public research, and experienced management. High heating costs in many temperate locations are also a problem. Although hourly labor rates are much lower in Mexico, typically lower labor productivity means that total labor cost savings are less than the differential in labor rates. Overall, at this stage, Mexico’s greenhouse tomato industry does not appear to have a clear advantage in unit costs.

Greenhouse Tomato Prices Falling

Despite rising demand for greenhouse tomatoes, the industry is facing downward price pressures, as demand growth has sometimes been outpaced by expanding supply. Two periods of very low producer prices had significant effects on the industry. In 1999, low grower prices for beefsteak tomatoes (a large, round, red tomato and the leading greenhouse product at the time) stung growers who had invested in greenhouses when prices were much higher. In response, greenhouse expansion faltered and some less profitable greenhouses were closed. Growers diversified their product mix by shifting to more tomatoes-on-the-vine, or cluster tomatoes. Between 1999 and 2003, the share of beefsteak tomatoes in the total retail quantity sold of fresh tomatoes fell from 18 to 13 percent, while the share of cluster tomatoes rose from 13 to 24 percent. But the rapid growth of cluster tomatoes led to overproduction in this segment and extremely low prices by the summer of 2004. The price drop is slowing further expansion in cluster tomatoes.

Production of the leading greenhouse tomato products—beefsteak and cluster—has now grown to the point where they are becoming mainstream commodities. For specialty niche products with limited supply, it is generally easier to command consistently high prices, in part because buyers place less emphasis on aggressive price negotiations for products that are not major contributors to the bottom line. But sales of greenhouse tomatoes are now critical to the profitability of overall retail tomato sales, and prices play a more influential role in purchasing transactions. Increasing competition drives down grower margins.

As the industry matures, greenhouse tomato growers strive for continual product innovation as a strategy for adding value, stimulating consumer interest, and maintaining margins and profitability. The expanding product line currently consists of smaller cluster tomatoes (such as cocktail tomatoes, including Campari), roma and mini roma cluster tomatoes, heirloom, and different-colored tomatoes. Greenhouse tomato producers tend to be closer to the pulse of consumers because they market a retail- and consumer-ready product. In addition, they increasingly market directly to retailers, rather than through intermediaries, such as repackers and wholesalers, as is the case for most field tomato shippers.

Impacts on Field Tomatoes Mixed

Competition from greenhouse tomatoes has brought major changes in the quantity and composition of field tomato sales. While total retail quantity sold of all fresh tomatoes increased from 1999 to 2003, the volume of field tomatoes declined after 2001, with the share falling from 69 to 63 percent. Over the same years, the share of all round tomatoes (mature green and vine ripe) declined from 43 to 31 percent (see “Field Tomato Variety Expands”). The roma share fell from 23 to 19 percent, but the grape and cherry category grew from 3 to 13 percent. Most grape and cherry tomatoes are field grown, mitigating the impact of greenhouse tomatoes on the field-grown category. Within the declining round category, the share of mature green tomatoes fell from 78 to 39 percent, with vine ripe tomatoes benefiting.

While mature green tomatoes are being forced out of the retail market by competition from both greenhouse and other field tomato types, they still dominate the expanding foodservice market, which represents about half of U.S. tomato consumption. With declining retail sales, the mature green industry is increasingly dependent on the foodservice market, where greenhouse tomatoes have not yet made significant inroads. However, this could change since some greenhouse firms have recently begun to experiment with developing an acceptable product for foodservice users.

If foodservice demand falters, mature green tomato growers would need to consider other alternatives, with serious industry structural adjustments likely. Growers could continue to attempt to reposition field tomatoes through new varieties, products, and packaging with more commercial appeal. Alternatively, the industry could diversify into the greenhouse industry, either through alliances with existing producers or through direct investment. However, greenhouse tomato production is very capital- and technology-intensive, creating barriers to entry. In addition, the rapid greenhouse expansion in the United States was accompanied by mixed profitability results; thus, most field tomato growers did not consider the greenhouse industry an attractive alternative. But recent profitability in the California field industry caused by weather-induced high prices may provide the financial wherewithal for some field growers to explore greenhouse production. If they were to invest, they would be new entrants in a maturing industry.

Greenhouse and Field Tomato Market Interactions Increase

In the early days of the evolution of greenhouse tomatoes, the greenhouse and field tomato sectors operated on a relatively independent basis. Now that they are a major market force, greenhouse tomatoes are increasingly influenced by supply and demand trends in the fresh field tomato industry, and vice versa.

In fall 2004, a weather-induced period of short supplies of fresh field tomatoes enabled greenhouse producers to benefit from a brief period of extraordinarily high prices as buyers substituted greenhouse for field tomatoes, where possible. In contrast, earlier in summer 2004, a record-high supply of greenhouse tomatoes caused greenhouse prices to decline, making them even more attractive to retail buyers, and placing a damper on demand for fresh field tomatoes. With greater supply has come an increased willingness on the part of consumers, retailers, and foodservice users to experiment with tomato types.

Developments in Mexico Will Shape the Future

Notwithstanding brief periods of abnormally high prices, average grower prices for greenhouse tomatoes have been trending downward. If this trend continues, some parts of the North American greenhouse tomato industry may become less viable. Growers will continue to seek the lowest cost production regions and form marketing alliances to build year-round supply. Greater competition means that new entrants have less room for error; the learning curve is shorter than in the 1990s, when the industry was in its infancy and average prices were higher. The greatest source of uncertainty for the future of the North American greenhouse tomato industry will be the changing structure of the Mexican industry, which is still seeking out the best locations, technology packages, and management practices. U.S. and Canadian growers will be following developments in Mexico closely when making their future investment and marketing decisions.

This article is drawn from:

- Cook, R. & Calvin, L. (2005). Greenhouse Tomatoes Change the Dynamics of the North American Fresh Tomato Industry. U.S. Department of Agriculture, Economic Research Service. ERR-2.