Federal Tax Policy Issues

Tax legislation enacted over the past two decades has reduced Federal income taxes for both individual and business taxpayers. Many of the enacted tax policy changes affecting both farm and nonfarm rural households were temporary. However, the American Taxpayer Relief Act of 2012 made many of the expiring tax provisions permanent. Most recently, the Tax Cuts and Jobs Act (TCJA), passed in December 2017, made several changes to the tax code. The TCJA temporarily eliminated or modified many itemized deductions and tax credits while lowering tax rates on individual and business income. The individual income tax provisions under the TCJA are temporary and apply for taxable years after December 31, 2017, and before January 1, 2026.

Although Federal estate and gift taxes account for a relatively small share of the Federal taxes paid by farm households, they may affect the ability of some farms to transfer the farm business to the next generation. In 2018, the TCJA doubled the previous estate tax exemption amount to nearly $11.2 million per individual but kept the 40 percent maximum marginal rate for 2018 and beyond. The TCJA maintains the previous law by allowing the basis in the property acquired from a decedent to be stepped-up to the value of the asset at the date of death.

Federal Income Tax and Farm Households

The Federal income tax is a progressive tax imposed on net income. Taxable income is computed by subtracting allowable adjustments, deductions, and personal exemptions from total income. Numerous Federal income tax law provisions allow taxpayers to reduce their tax liability if they undertake certain tax-favored activities. Farmers benefit from both general tax provisions available to all taxpayers and provisions specifically designed for farmers.

Farmer-specific tax benefits tend to accrue for farms with higher incomes, which are generally large farms with high farm income and very small farms with high levels of off-farm income. Although very small farms do not generate enough farm income to support a family, most small farms benefit from their ability to claim farm losses for tax purposes because these losses can be used to offset nonfarm income and thereby reduce overall taxes. At the same time, some farmers working full-time on farming operations do not generate enough taxable income—either farm or nonfarm—to fully use the available tax benefits.

Examples of special tax treatment for farmers include cash accounting (or cash method), multi-year averaging for farm income, accelerated depreciation, and capital gains treatment for certain assets used in farming. (For definitions of tax terms, see the IRS website.) These and other provisions reduce the farm income tax base. Such incentives have likely encouraged greater investment in productive capacity than would have occurred without tax incentives, and this may have affected farmland prices, organizational structure, and farm profitability.

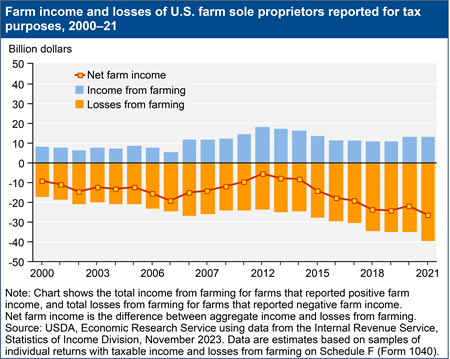

The favorable tax treatment for farm income is reflected in the size of farm income and losses reported for income tax purposes. Since 1980, Internal Revenue Service data indicate sole farm proprietorships have reported a combined negative net farm income for tax purposes (see Statistics of Income, taxable profit and losses from farming, Schedule F (Form 1040)). These farm losses reduce taxes by offsetting taxable income from nonfarm sources.