Concentration in U.S. Meatpacking Industry and How It Affects Competition and Cattle Prices

Highlights:

-

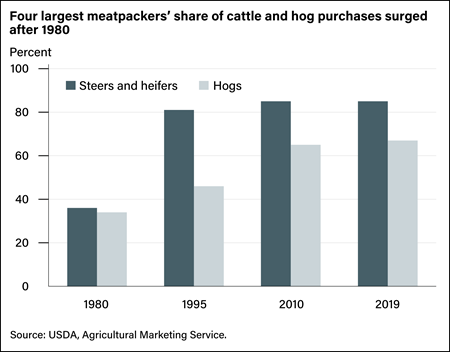

Meatpacking is a concentrated industry, with the four largest firms handling 85 percent of all steer and heifer purchases and 67 percent of all hog purchases. High concentration, and its links to competition, is a focus of recent policy initiatives aimed at encouraging more competition.

-

Meatpacking industries concentrated rapidly in the 1980s and 1990s. An outpouring of research followed and found only limited evidence that high packer concentration caused reduced prices for livestock.

-

However, in recent years there is evidence of reduced competition in meatpacking, with lower prices for cattle. This evidence is reflected in sharply increased spreads between cattle prices and wholesale beef prices, the disappearance of excess capacity in packing plants, and recent entry into the industry by new packers. Entry and capacity expansion could encourage renewed competition in the industry.

Meatpacking is a concentrated industry, with a few firms accounting for most production. Across the entire U.S. economy as well as in agribusiness, industry concentration has reemerged as a policy issue. In 2020, the House Committee on Agriculture directed USDA to investigate the vulnerability of the beef supply chain and the level of concentration in the industry. In 2021, President Biden issued an Executive Order, “Promoting Competition in the American Economy,” which referred specifically to meatpacking concentration and its effects on financial returns to farmers and ranchers. In 2023, the Federal Trade Commission and the U.S. Department of Justice—charged with enforcing the Nation’s antitrust laws—jointly issued revisions to their “Merger Guidelines” aimed at concentration in U.S. industries.

The broad policy questions over concentration involve how it affects competition within industries. Can firms in highly concentrated industries use their market power to raise prices to buyers while reducing the prices they pay suppliers and the wages they pay workers? At the same time, does a lack of competitive rivalry protect inefficient producers and lead to reduced innovation? These broad questions have been closely studied in meatpacking. After rapid increases in industry concentration during the 1980s, Congress funded research into its causes and consequences during the 1990s and 2000s. In 2010, USDA and the U.S. Department of Justice held a series of joint public workshops on concentration and competition in agribusiness, with a significant focus on meatpacking. Currently, there is stronger evidence of market power in the meatpacking industry.

Concentration in Meatpacking

Meatpacking industries underwent striking change over the past 40 years. In 1980, the four largest beef packers accounted for 36 percent of all purchases of steers and heifers, while the four largest pork packers (a different group of firms) accounted for 34 percent of all purchases of market hogs. By 1995, the largest four firms accounted for 81 percent of steer and heifer purchases. Concentration in hogs grew more slowly, but by 2019 the four largest packers accounted for 67 percent of all hog purchases. This concentration of production among fewer packers means there are fewer firms buying livestock. In most parts of the country, ranchers and farmers now have two to four buyers for their cattle or hogs.

Concentration increased in large part because packers built bigger plants. In 1980, the average beef-packing plant owned by one of the top four firms handled 417,000 cattle; by 2002, that average plant size had more than doubled to more than 1 million head. Hog packers also built much larger plants: Nearly 90 percent of all hogs moved through plants handling at least 1 million hogs a year by 1997, compared with 38 percent just 20 years before.

Bigger plants provided firms with economies of scale, as a larger volume of livestock resulted in lower per-animal processing costs than smaller plants. The new plants required large and steady flows of animals to realize those economies, and packers moved to assure a dependable supply of livestock by creating tighter coordination with cattle and hog producers through direct ownership or contracts.

The industry’s consolidation raised questions about competition, particularly as it related to prices paid for cattle and hogs. With fewer firms competing with one another, would packers be able to reduce the prices they paid to farmers and ranchers compared with a world with more (and smaller) competing firms? On the other hand, those fewer firms also had lower processing costs, which they could pass on to beef and pork consumers. Lower consumer prices could then lead to increased consumption, higher demand for cattle and hogs, and higher prices to farmers and ranchers. Studies completed in the 1990s and 2000s, funded with congressional and USDA support, aimed to answer those questions, with a focus on cattle markets.

That research found the industry’s shift to larger plants led to increased concentration and to lower production costs. In turn, lower production costs did translate into lower consumer prices, increased consumption, and higher prices for cattle and hogs. However, with fewer rivals because of increased concentration, most of the studies found packers were also able to exercise some market power and pay lower prices for cattle than they would have had they faced more competitors. Even so, the impact of higher concentration—reducing prices paid for cattle—was more than offset by the impact of lower production costs on raising cattle prices.

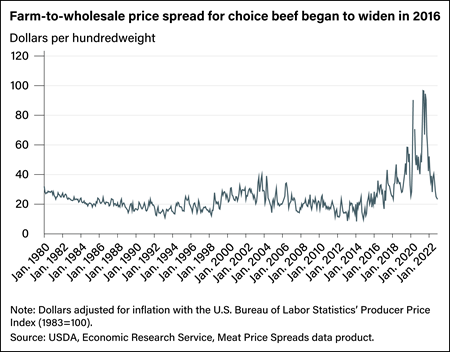

The findings can be illustrated with the Meat Price Spreads data product produced by USDA’s Economic Research Service. The farm-to-wholesale choice beef price spread is the difference between the average monthly price paid by packers for choice-graded cattle and the wholesale value received by packers for the beef and byproducts produced from the animals. The spread therefore encompasses the packers’ processing costs and profits. If increased concentration in the 1980s and 1990s provided packers with greater market power, price spreads should have risen in that period.

Instead, while the data show sharp month-to-month fluctuations, there also is a clear trend during the 1980s and 1990s. As production shifted to the larger plants built during this period, and as per-animal processing costs fell, the spread between cattle and wholesale beef prices declined. If the packers were able to exercise substantial market power in the 1980s and 1990s, it does not appear in the spread (or in more sophisticated statistical analyses).

Spreads grew in the early 2000s, as the shift to larger plants with lower costs was largely completed and production costs stopped declining. Spreads narrowed again after 2005. From 1980 to 2015, it is hard to see any persistent increase in the farm-to-wholesale spread, even as industry concentration increased to high levels.

The price spread showed much larger month-to-month fluctuations after 2015, associated with impactful but temporary developments, such as packing plant closures because of a fire and the Coronavirus (COVID-19) pandemic (as plant workers caught the virus). However, the series also shows a strong trend increase, to double and triple the average values in years prior to 2016. While wages in meatpacking plants rose faster than overall inflation, only a small part of the spread’s increase can be attributed to rising costs at packing plants. Something appears to have changed after 2015.

What Happened After 2015?

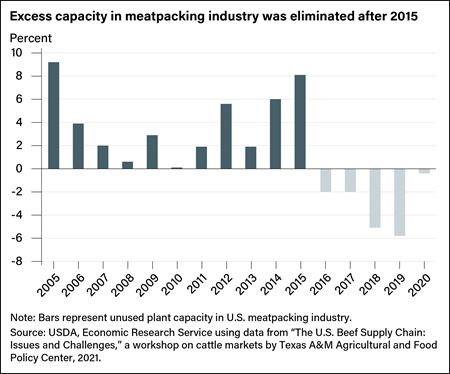

The increase in the farm-to-wholesale choice beef price spread coincided with another market development, the disappearance of excess capacity in the industry. In the meatpacking industry, firms design plants with a specific capacity in mind, and the plants can produce under that capacity. They also can produce more than their designed capacity by adding evening and weekend shifts.

When the industry is operating below capacity, packers have an incentive to bid aggressively for cattle. Firms incur capital and labor costs whether the plant is fully in use or not. A plant will then incur only small additional costs for processing 50 to 100 more cattle when operating under capacity, and they can make money on that extra lot of cattle even when paying more than they paid for the rest of their cattle. What’s more, extended periods of operating under capacity affect company strategies, as packers and their cattle buyers develop routines to persistently search and bid aggressively for additional cattle to run through the plant.

During the industry’s late 20th century consolidation, U.S. beef consumption and production grew slowly. A decline in per capita consumption was only partly offset by a growing U.S. population and rising beef exports, and total U.S. beef production in 2015 was only 5 percent greater than it was in 1977. As a result, actual production in U.S. beef plants often fell well below the plants’ designed capacity. The industry operated below capacity every year from 2005 through 2015, and other evidence indicates it operated below designed capacity before 2005 as well. By 2015, excess capacity amounted to 8 percent of the industry’s designed capacity.

Over time, the industry gradually reduced its designed capacity as small and midsize packing plants closed. Those plants faced higher per-animal processing costs and could not operate profitably in a competitive environment for cattle purchases. As capacity gradually shrank, actual production grew—although slowly—and by 2016 packers were adding extra weekday and Saturday shifts to use plants more intensively and to generate production above designed capacity.

When plants run at or above capacity, increasing production raises labor expenses because plants must pay workers overtime to fill extra shifts. The increased workload also adds capital maintenance and replacement expenses as equipment is used more intensively. Meatpackers and their buyers are then less likely to bid higher for additional cattle, and in extended periods of full capacity they can adjust strategies to bid less aggressively on all the cattle they buy. This helps account for the wide expansion in spreads after 2015.

Market Adjustments: Entry into Meatpacking

Rising spreads, if they reflect increased profits for meatpackers, should lead to market adjustments as existing packers expand plants and new firms enter the business. Recently, there has been evidence of both. One of the top four packers added capacity at its plants, and a second bought another plant and announced plans to expand it, before suspending those plans in the face of rising construction costs in 2022. However, the major source of capacity expansion is coming from expansions by smaller firms and entry by new producers.

Seven firms have announced plans to build new beef-packing plants since 2021, and four other small firms have announced expansions of existing plants. Few of the plants have opened yet, and most are under construction. However, if all the planned new and expanded plants open, they will represent an aggregate increase in industry capacity of more than 13,000 cattle per day, or about 3.3 million cattle per year at normal operating routines. That amounts to nearly 13 percent of all steers and heifers slaughtered in 2022, a substantial capacity expansion that, if fully carried out, could result in higher prices paid for cattle and reduction of price spread.

| Firms entering the meatpacking industry or expanding existing plants since 2021 | ||

|---|---|---|

| Firm | Plant location | Designed capacity |

| Plant openings | ||

| Producer Owned Beef | Texas | 3,000 head/day |

| American Food Groups | Missouri | 2,400 head/day |

| Cattlemen’s Heritage | Iowa | 2,000 head/day |

| Sustainable Beef | Nebraska | 1,500 head/day |

| Missouri Prime (STX) | Missouri | 750 head/day |

| Intermountain Packing | Idaho | 500 head/day |

| True West Beef | Idaho | 500 head/day |

| Plant expansions | ||

| Upper Iowa Beef | Iowa | 1,000 head/day expansion |

| Greater Omaha Packing | Nebraska | 700 head/day expansion |

| FPL Food | Georgia | 500 head/day expansion |

| Riverbend Meats | Idaho | 300 head/day expansion |

| Source: USDA, Economic Research Service calculations from reports in trade magazines. | ||

There are several notable features of these investments. First, groups of cattle feeders and ranchers are building most new plants. Their entry into packing, and the substantial capital commitments implied, indicate they could be dissatisfied with the services provided and prices received from existing packers.

Second, USDA has provided support for capacity expansion since 2022 under the department’s Meat and Poultry Processing Expansion Program. The largest packers are not eligible for the grants, which are intended to support expanded competition through new and expanded processing and slaughter facilities for many types of animals. Some of the firms building beef packing plants have received grants from the USDA program for up to $25 million per plant. New beef plants require significant capital investments, on the order of $300 million for a plant with a designed capacity of 1,500 head per day. Thus, the USDA program provides additional support for those projects in addition to private debt and equity funding. The novelty of the USDA program lies in the fact that it does not rely on traditional antitrust interventions to promote competition, but instead aims to directly address the capacity constraints that have recently hindered competition in the industry by providing additional capital to new and smaller producers.

Third, the new plants are relatively small. Large plants are designed to handle around 5,000 cattle per day, while the new plants are designed to handle 500 to 3,000 head per day. At those sizes, the smaller firms may produce at higher per-head costs than the large packers. The smaller firms are pursuing several strategies to offset those cost risks. Some will focus on niche markets for high-quality beef sold at premium prices. Others aim to use contractual commitments with their rancher/feeder owners to provide steady flows of cattle through the plants, thus operating as efficiently as possible. Firms also aim to obtain long-term purchase commitments from beef buyers, and one has entered an alliance with the Nation’s largest food retailer. Nonetheless, the new entrants face financial risks if their entry leads to excess industry capacity and shrinking farm-to-wholesale price spreads.

Concentration and Competition: Lessons from Meatpacking

The meatpacking industry provides several insights for discussions of concentration and competition in the broader economy.

Changes in industry concentration often reflect important underlying changes in an industry’s organization, changes that frequently lead to lower costs, improved productivity, and benefits for consumers and suppliers. In meatpacking, the changes were the realization of scale economies through larger plants and the associated shift to closer coordination with livestock suppliers. Those organizational changes, when combined with slow growth in beef consumption, led to increases in concentration, accompanied by lower per-animal processing costs.

What is more, higher concentration does not necessarily imply reduced competition. Even with the increases in concentration in meatpacking between 1980 and 1995, spreads between prices paid to ranchers and wholesale prices charged to meat buyers did not grow. Moreover, more sophisticated statistical analyses did not find evidence of reduced competition in livestock markets in that period.

However, high concentration can combine with other factors to limit competition. Trends in farm-to-wholesale spreads since 2016 suggest that packers have been able to reduce prices paid for cattle with help from a combination of high concentration and limited packing plant capacity. The efforts of ranchers and cattle feeders to enter packing with plants of their own further suggests a deterioration of competition in recent years as it indicates dissatisfaction with the prices that ranchers and feeders have been receiving from packers.

Finally, the recent construction of new plants points to another element in evaluations of industry competition: The effect of concentration on competition and pricing also depends on the ease with which new rivals may enter the industry and provide new competition for existing firms.

Concentration and Competition in U.S. Agribusiness, by James M. MacDonald, Xiao Dong, and Keith Fuglie, ERS, June 2023

Consolidation in U.S. Meatpacking, by James M. MacDonald, Michael Ollinger, Kenneth Nelson, and Charles Handy, USDA, Economic Research Service, March 1999

Meat Price Spreads, by William Hahn, USDA, Economic Research Service, April 2024

Beef and Pork Values and Price Spreads Explained, by William Hahn, USDA, Economic Research Service, May 2004