Under the Tax Cuts and Jobs Act, Only 0.11 Percent of Farm Estates Would Have Owed Estate Taxes in 2016

For nearly a century, the Federal estate tax has applied to the transfer of property at death. Recently passed in December 2017, the Tax Cuts and Jobs Act (TCJA) not only changed the Federal income tax system but also doubled the estate tax exemption amount to $11.18 million per individual. This exemption amount has increased significantly since 2000, when the exemption was $675,000, resulting in fewer farm estates that must file a tax return or that owe estate taxes.

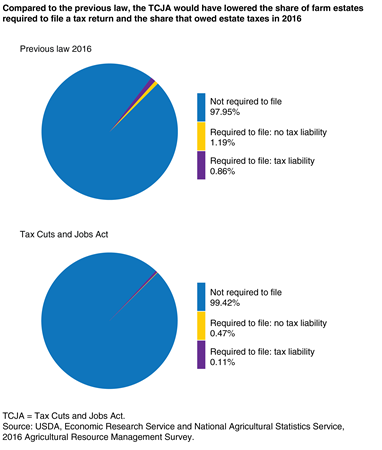

Using an actuarial model and data from USDA’s Agricultural Resource Management Survey, ERS researchers estimated that 39,214 farm estates were created in 2016. Had the TCJA been in effect in 2016, only 0.58 percent of these farm estates would have been required to file an estate tax return. After accounting for adjustments, deductions, and expenses, only 0.11 percent of these estates would owe estate taxes. Across all estates that owe tax, the aggregate liability was estimated at $104 million.

By comparison, under the previous law in 2016, ERS estimated that 2.05 percent of farm estates were required to file an estate tax return, but only 0.86 percent of farm estates would owe estate taxes. Across all estates that owe tax, the aggregate liability was estimated at $496 million in 2016.

Estimated Effects of the Tax Cuts and Jobs Act on Farms and Farm Households, by James Williamson and Siraj G. Bawa, ERS, June 2018

Federal Tax Issues, by Tia M. McDonald, USDA, Economic Research Service, April 2024

Federal Tax Policies and Farm Households, by Ron Durst, USDA, Economic Research Service, May 2009