Market Outlook

See the latest Livestock, Dairy, and Poultry Outlook report.

Summary

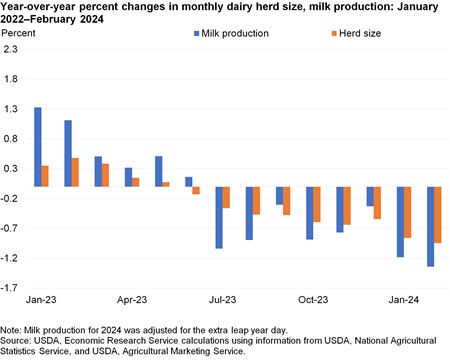

Dairy: The 2024 milk production forecast has been lowered to 226.3 (-1.0) billion pounds due to slower anticipated milk yield per cow, with cow numbers remaining unchanged. Dairy product price forecasts show mixed changes from last month’s forecasts with Cheddar cheese at $1.620 (-9.0 cents), dry whey at $0.425 (-2.5 cents), butter at $2.925 (+12.5 cents), and nonfat dry milk (NDM) at $1.180 (-3.0 cents) per pound. The Class III milk forecast is now $16.20 per hundredweight (cwt), down $0.95 due to lower cheese and dry whey prices. Despite lower NDM price forecast, the Class IV price forecast has risen to $20.40 per cwt, up $0.30 due to higher butter prices. The all-milk price for 2024 is projected at $20.90 per cwt, down $0.35 from the previous month’s forecast.

Download chart data in Excel format.